After The SpaceX And Cursor Deal: What Might Change?

After The SpaceX And Cursor Deal: What Might Change?

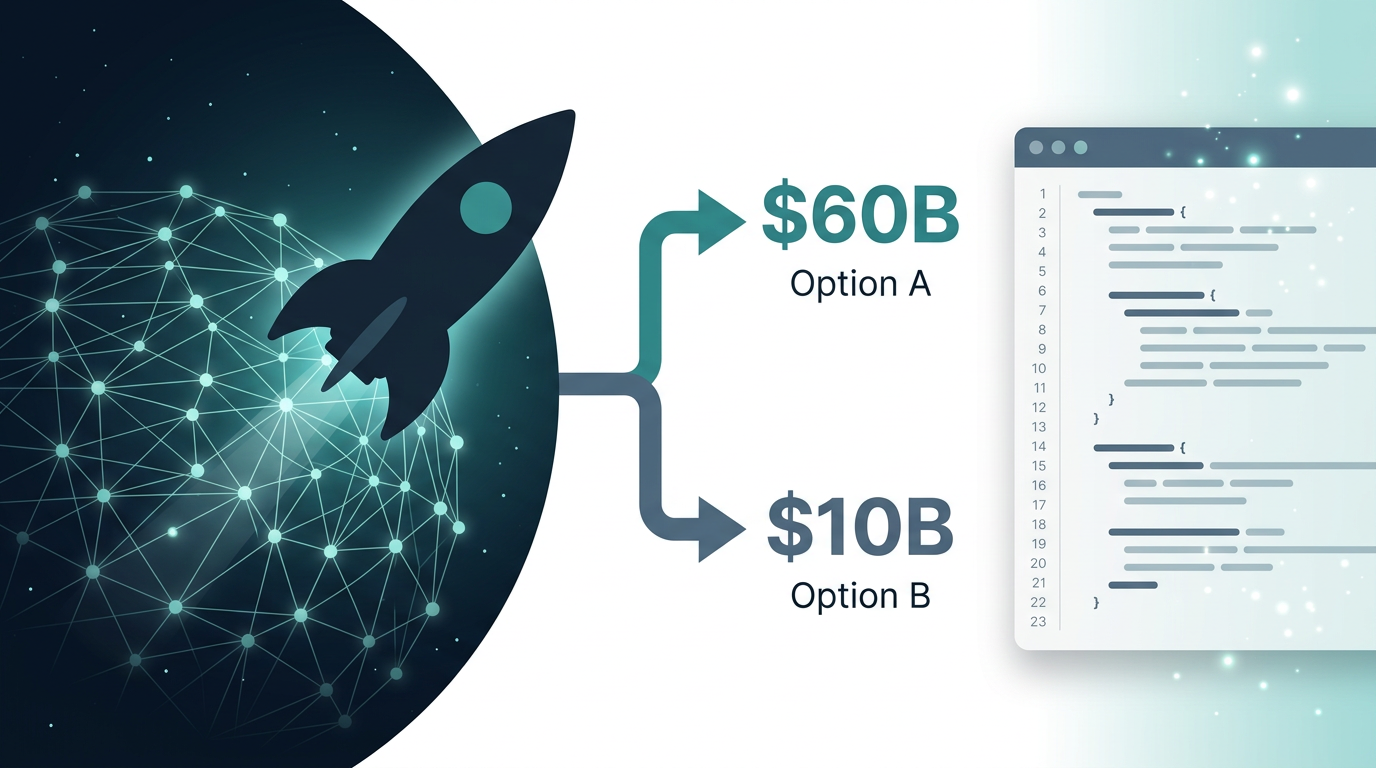

Reports from TechCrunch, The Verge, and The New York Times described a striking arrangement: SpaceX and Cursor’s parent company Anysphere would work together on models for “programming and knowledge work.” Later in the year, SpaceX reportedly has two choices: acquire the company for about $60 billion, or pay around $10 billion for the collaboration if the acquisition does not happen.

The industry had already seen related background chatter: xAI computing resources for Cursor training, and some important Cursor engineering talent moving toward xAI. Chinese media also picked up the story quickly. What interests me most is not the headline number, but this question: if the acquisition happens, what changes in the AI coding battlefield? Model sourcing, product shape, and regional availability may all shift.

What The Reported Agreement Says

The points repeated across reports and platform discussions are roughly these:

- Cursor’s product and distribution among professional developers would be combined with SpaceX’s reported Colossus large-cluster compute, aiming at a very strong programming and knowledge-work model.

- Cursor still sells access to, and integrates with, external models such as Claude and GPT. At the same time, OpenAI and Anthropic are pushing their own coding tools to the same paying users.

- The deal structure is unusually eye-catching: either an acquisition later, or a large collaboration payment. The Verge put it plainly: breakup fees are not unusual, but public framing around “$10 billion for AI we build together” stands out.

Cursor, Claude Code, Codex, And Copilot

All these products target programmers or product builders willing to pay for AI-assisted coding, but their product shapes differ a lot.

Cursor is effectively an AI-specialized editor, derived from VS Code. Its strengths are multi-file work, indexing, and long sessions inside an IDE. Historically, the model layer often felt like a switchable engine: users paid Anysphere mainly for the tool and workflow, not directly for one foundation model. Cursor’s initial impression was not “we own a base model that can fight Claude and OpenAI head-on.” Its advantages were ease of use, fast iteration, and enterprise willingness to buy.

Claude Code from Anthropic is more of a terminal / agent product tightly bound to Anthropic’s own model ability. Its strengths are long context, instruction following, and complex long-running tasks. In that sense, it is a good example of model as product.

OpenAI Codex, together with ChatGPT, IDE extensions, and CLI directions, is closely tied to OpenAI’s model and product brand. The ecosystem also includes GitHub Copilot, an older and deeply distributed product inside GitHub and Visual Studio. OpenAI and Anthropic both have flagship models and their own top-tier coding tools, while also serving models to Cursor. Even with the same model family, the product experience and policy surface will not be identical. That is Cursor’s long-term awkward position.

At the moment, Cursor feels product-strong but model-weaker. Its Composer 2 model, based on Kimi K2.5, is quite usable, but still not at the level many users expect from flagship Opus or GPT releases.

What People Are Actually Discussing

On overseas platforms, several topics repeat:

- The $60B / $10B framing, seen together with Cursor’s fundraising and valuation discussions, looks like a strong pre-IPO story.

- Whether Cursor’s model path will tighten around xAI. If compute and equity narrative both point toward SpaceX / xAI, default models, enterprise contracts, and training-data policy may become more constrained.

- How Cursor competes with official coding tools from OpenAI, Anthropic, Google, and others. This is not only a Cursor story; it is the whole coding-agent track getting more crowded.

- Whether independent developers benefit. A stronger in-house model and more stable compute would help. But if model choice narrows or prices rise, complaints will come.

In Chinese technology media and social platforms, the discussion adds several local concerns:

- Arguments around self-developed models, base models, wrappers, and licensing history. This is separate from the acquisition story, but it affects whether people trust Cursor’s long-term reliability.

- Pressure on domestic IDEs and plugin ecosystems. If model and compute concentrate around a few American players, local toolchains, compliance, and procurement become harder topics.

The official Cursor forum thread, such as Anysphere’s explanation of current developments, should be read alongside media reports. What the company promises, and what it does not promise, matters more than secondhand interpretation.

The next question people ask is usually this: can Cursor use the collaboration to fill its biggest gap with a demonstrably strong in-house model plus exclusive compute? If yes, comparisons with Claude Code and Codex change dramatically. If not, Cursor remains more like the smoothest tool, living on product and channel strength.

For Users Outside The US

Different tools carry different account, payment, and regional policy surfaces.

Claude / Anthropic products have long generated community discussion around availability, account verification, and payment reliability. The rules change, so I will not pretend to make a final judgment here. The point is simpler: for someone who just wants to write code quietly, every extra uncertainty becomes friction. If Claude Code is tied tightly to Anthropic’s higher-tier membership and terminal tool, that front door remains part of the experience.

OpenAI / ChatGPT Plus / Codex routes depend on OpenAI account and product policy. Payment and regional availability issues follow that same path.

Cursor has often felt easier to start for many individual developers: install the editor, subscribe through the available payment path, and start working. That convenience is part of why it deserves separate discussion. It is not a question of which tool is more prestigious; it is about which part of the workflow fights you least.

If the SpaceX / US-capital side becomes a deeper binding or an acquisition, several possibilities are worth watching. These are not predictions, just directions of concern:

- Billing and payment: If the receiving entity, tax rules, invoices, and refund policy align more closely with large US technology companies, the current convenience may change.

- KYC, team plans, and enterprise contracts: Larger enterprise procurement usually brings real-name requirements, corporate contracting, and data-residency discussions. Personal informal usage may become less central.

- Regional terms and service policy: Any parent group under US export-control, sanctions, or service-region constraints may reflect that in terms of service. No one can guarantee otherwise based only on this news. Individual developers who rely on Cursor should occasionally read official announcements, not wait for the client to show a red warning one day.

Putting this together with the earlier tool comparison: Cursor is currently easy to board. If models and capital become more American and more single-stack, it may become a SaaS where you must accept a larger business and compliance model to get the best capability. Then comparison with Claude Code and Codex is no longer only about model strength. It is also about accounts, payment, and procurement friendliness for your location and team.

Closing Thoughts

Deal details will change, and model rankings will change too. What I care about is:

- Whether Cursor moves from “multi-model shell” toward “self-developed model plus compute story.”

- Whether the competition with Claude Code and Codex shifts from plugin comparison to full-stack comparison.

- Whether users who are used to simple subscription flows suddenly face more account, billing, or policy steps.

The first two can be tracked through TechCrunch, The Verge, official forums, and release notes. The third requires paying attention to account emails and billing pages.

References

- SpaceX is working with Cursor and has an option to buy the startup for $60B - TechCrunch

- SpaceX cuts a deal to maybe buy Cursor for $60 billion - The Verge

- The New York Times related report

- Cursor forum: Anysphere explanation thread

- 36Kr background report

- NetEase syndicated example

Follow ZiCode on WeChat

If this post was useful, you can follow later updates on WeChat as well.

X / Twitter

Follow @ax2_zicode

Faster technical notes, short thoughts, and new-post alerts are posted on X.